We asked Viston to modernize our fraud detection and AML monitoring with explainable AI and graph analytics while meeting regulator expectations.

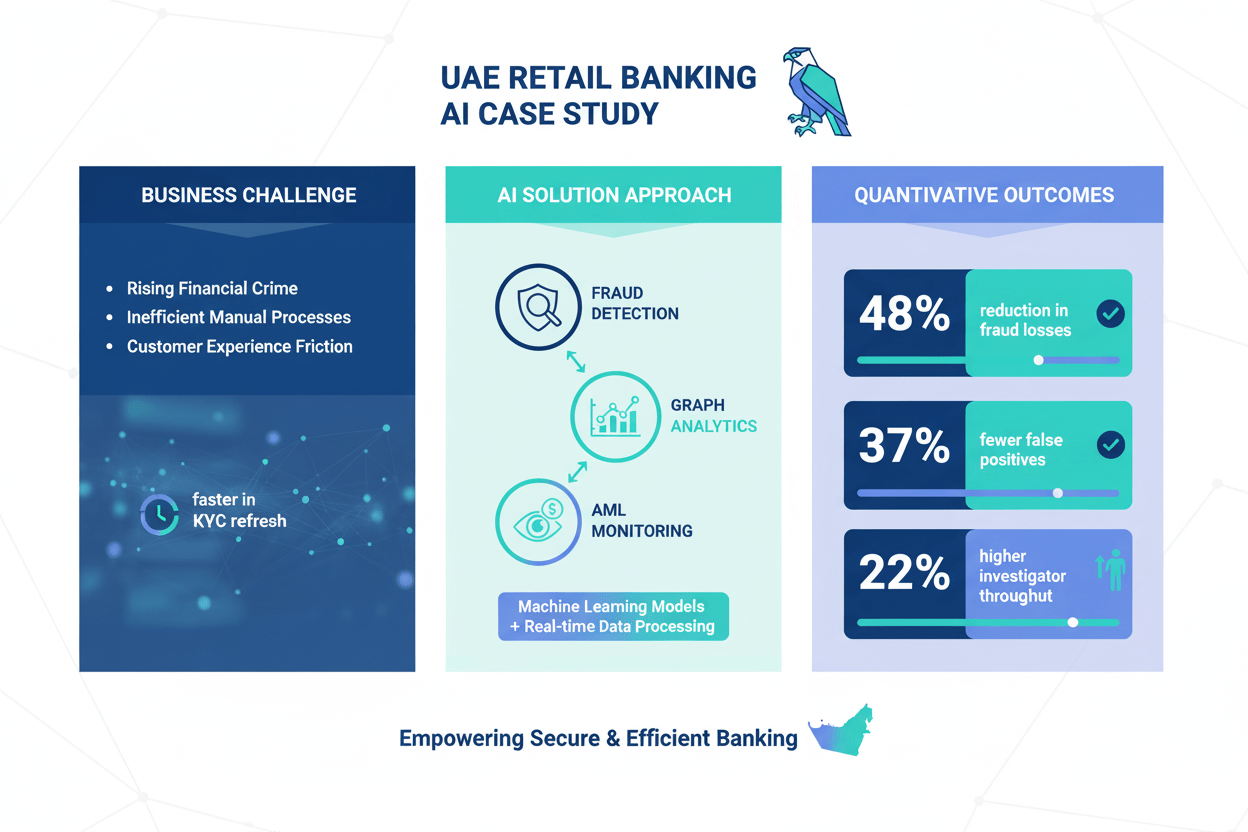

Business challenge

- High false positives in card fraud, rising mule activity, and manual KYC refresh.

- Fragmented rule engines and limited case investigation tooling.

Our approach and solution

- Built a streaming fraud scoring pipeline with graph features and explainable models.

- Upgraded AML monitoring with entity resolution and risk scoring; automated KYC refresh.

AI applications and benefits delivered

- Real-time fraud scoring with LightGBM and graph-derived features.

- Neo4j-based network risk scores to surface mule rings.

- SHAP-based explanations integrated into case management.

- LLM assistant for investigator summarization and SAR drafting with strict guardrails.

Cost of implementation

- USD 1,75,000 including data platform uplift and model validation.

Time to implement

- 7 months to full production across cards and retail payments.

Tools and technologies used

- Azure Databricks, Spark Structured Streaming, Kafka, Snowflake, Neo4j, LightGBM, SHAP, Elastic Stack, AKS, Key Vault, MLflow, Great Expectations, Power BI.

Quantitative outcomes

- 48% reduction in fraud losses on targeted products.

- 37% reduction in false positives.

- 60% faster KYC refresh turnaround.

- 22% higher investigator throughput.

Key performance indicators (KPIs) tracked

- Fraud loss rate bps, false positive rate, precision/recall, time-to-detect, AML alert productivity, SAR timeliness, model drift.

Pre- and post-implementation metrics

- Fraud loss rate: 7.8 bps → 4.1 bps.

- False positive rate: 92% → 58%.

- Average KYC TAT: 10 days → 4 days.

- Alerts per investigator per day: 18 → 22.

Stakeholder quotes or testimonials

- “Explainability made model sign-off straightforward with internal audit and the regulator.” — Head of Financial Crime.

- “Graph features exposed mule networks we couldn’t see with rules only.” — Fraud Strategy Lead.

Regulatory or compliance considerations

- UAE Central Bank AML/CFT guidance, FATF-aligned controls, PCI DSS scope containment, model risk policy adherence, challenger model testing, comprehensive audit logs, privacy-by-design.